CMA考试与认证

CMA考试与认证

发布时间:2019-01-02

发布时间:2019-01-02

以下内容大纲代表了CMA考试将涵盖的知识体系。当新的内容成为行业共识时,大纲将会随之更新。

CMA认证的考生必须参加并通过第一部分和第二部分的考试。考生有责任了解大纲所涵盖领域的最新进展。这包括理解会计组织发布的公开声明,以及了解当前会计,财务和商业期刊中有关报告的最新进展。

考试内容大纲有多项用途。本大纲旨在:奠定考试的基础。为每次考试范围的一致性提供基础。详述考试各部分的内容。协助考生准备各部分考试。

下面列出了有关内容大纲和考试的其他重要信息。

1.大纲中每个主题所占的百分比代表该主题在考试中的相对权重。每个主题的考题数量占总题量的比例与此权重相近。

2.考题的分布取决于所考察主题的相对权重。每个主题下的考点没有再次分配相对权重,不应根据考点的排列顺序或考点数量来推断其相对权重或重要性。

3.每个主题都有特定的难度水平,表示该主题所出题目的深度和广度,可以考

察从初级了解(A级难度)到透彻理解和应用的能力(C级难度)。关于考题的难度水平和对考生能力的具体要求,之后有详细的说明。

4.考点经过精心选择以尽量减少第一部分考试和第二部分考试内容的重叠。考题可涵盖本部分内的主题和主题内的相关考点。

5.关于美国联邦所得税的问题,考生在报告和分析财务结果时应理解所得税的影响。此外,还将测试影响决策(例如折旧,利息等)的有关税法规定。

6.CMA认证的考生也应了解财务报表编制,商业经济学,货币的时间价值,统计和概率的有关知识。

7.第一和第二部分考试分别为四小时,每个部分的考试包含一百个多项选择题和两个情境题。考生将有三个小时完成多项选择题,一个小时完成情境题。每项考试中含有少数供将来使用的测试题,这些题将不会计入最终得分。

8.情境题需要语言论述和计算解答。要求考生以合乎逻辑的方式回答问题,并证明对该问题的正确理解。为了更清楚地定义考生所需的考点知识,CMA考试对内容大纲中主要考点确定了不同层次的能力要求。成功的考生应具备的并将在考试中被测试的认知能力如下所示:

了解:记忆以前学过的材料,例如具体的事实,标准,技术,原则和过程(即识别,定义,列举)。

理解:掌握和解释材料含义的能力(即分类,解释,区分)。

应用:能够在新的和具体的情况下使用习得的材料(即证实,预测,解决,修改,关联)。

分析:能解构材料,理解其组织结构;能识别因果关系;区分行为,并识别与判断验证相关的元素(即区分,估计,排序)。

综合:能够将各部分放在一起形成一个新的整体或提议一种新的运作;能够将想法联系起来并形成假设(即结合,制定,修改)

评价:能依据一致性,逻辑准确性,和与标准的比较来判断给定项目的价值;能够对所作出的判断进行评估(即批评,辩解,结论)。

考题难度分为三个级别,分别定义如下:

Level A:Requiring the skill levels of knowledge and comprehension.

A级:要求了解和理解的能力。

Level B:Requiring the skill levels of knowledge,comprehension,

application,and analysis.

B级:要求了解,理解,应用和分析的能力。

Level C:Requiring all six skill levels,knowledge,comprehension,

application,analysis,synthesis,and evaluation.

C级:要求所有六种能力,了解,理解,应用,分析,综合和评

价的能力。

The levels of coverage as they apply to each of the major topics of the Content

Specification Outlines are shown on the following pages with each topic listing.The

levels represent the manner in which topic areas are to be treated and represent ceilings,

i.e.,a topic area designated as Level C may contain requirements at the“A,”“B,”or“C”

level,but a topic designated as Level B will not contain requirements at the“C”level.

下页中列举了大纲中的各主题的难度级别。所示级别为该主题考题能出现的最高难度,即指定为C级的主题可能出现“A”,“B”或“C”难度级别的题目,但指定为B级的主题不会出现“C”级的题目。

CMA考试内容概观

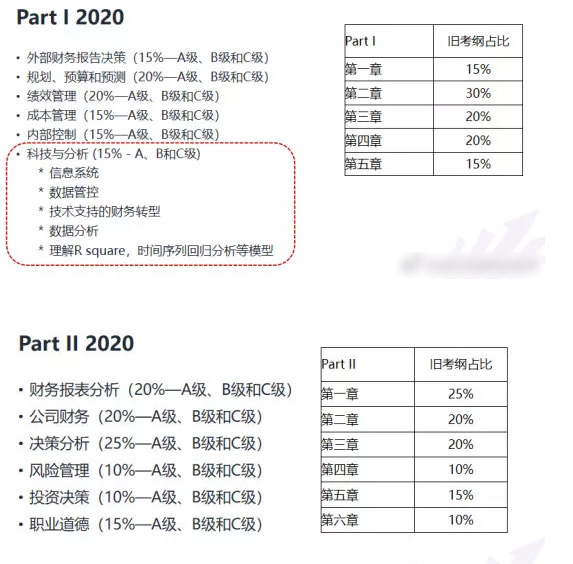

Part 1 Financial Planning,Performance,and Analytics

第一部分财务规划、绩效与分析

(4 hours–100 questions and 2 essay questions)

(4小时–100个选择题和2个情境题)

External Financial Reporting Decisions 15%Level C

Planning,Budgeting,and Forecasting 20%Level C

Performance Management 20%Level C

Cost Management 15%Level C

Internal Controls 15%Level C

Technology and Analytics 15%Level C

外部财务报告决策15%C级

规划、预算和预测20%C级

绩效管理20%C级

成本管理15%C级

内部控制15%C级

科技与分析15%C级

Part 2 Strategic Financial Management

第二部分战略财务管理

(4 hours–100 questions and 2 essay questions)

(4小时–100个选择题和2个情境题)

Financial Statement Analysis 20%Level C

Corporate Finance 20%Level C

Decision Analysis 25%Level C

Risk Management 10%Level C

Investment Decisions 10%Level C

Professional Ethics 15%Level C

财务报表分析20%C级

公司财务20%C级

决策分析25%C级

风险管理10%C级

投资决策10%C级

职业道德15%C级

Institute of Certified Management Accountants

Content Specification Outlines

Certified Management Accountant(CMA)Examinations

注册管理会计师(CMA)考试内容大纲

Part 1-Financial Planning,Performance,and Analytics

第一部分-财务规划、绩效与分析

A.External Financial Reporting Decisions(15%-Levels A,B,and C)

外部财务报告决策(15%-A、B和C级)

1.Financial statements

财务报表

a.Balance sheet

资产负债表

b.Income statement

利润表

c.Statement of changes in equity

所有者权益变动表

d.Statement of cash flows

现金流量表

e.Integrated reporting

综合报告

2.Recognition,measurement,valuation,and disclosure

确认,计量,计价和披露

a.Asset valuation

资产计价

b.Valuation of liabilities

负债计价

c.Equity transactions

权益性交易

d.Revenue recognition

收入确认

e.Income measurement

收益计量

f.Major differences between U.S.GAAP and IFRS

美国公认会计原则与国际财务报告准则的主要差异

Institute of Certified Management Accountants

B.Planning,Budgeting and Forecasting(20%-Levels A,B,and C)

规划、预算和预测(20%-A、B和C级)

1.Strategic Planning

战略规划

a.Analysis of external and internal factors affecting strategy

分析影响战略的内部和外部因素

b.Long-term mission and goals

长期使命与目标

c.Alignment of tactics with long-term strategic goals

根据长期战略目标调整策略

d.Strategic planning models and analytical techniques

战略规划模型与分析技术

e.Characteristics of successful strategic planning process

成功的战略规划制定过程所具备的特性

2.Budgeting concepts

预算概念

a.Operations and performance goals

经营和业绩目标

b.Characteristics of a successful budget process

成功的预算编制流程所具备的特性

c.Resource allocation

资源分配

d.Other budgeting concepts

其他预算概念

3.Forecasting techniques

预测技术

a.Regression analysis

回归分析

b.Learning curve analysis

学习曲线分析

c.Expected value

预期值

Institute of Certified Management Accountants

4.Budgeting methodologies

预算方法

a.Annual business plans(master budgets)

年度企业计划(总预算)

b.Project budgeting

项目预算

c.Activity-based budgeting

作业预算编制

d.Zero-based budgeting

零基预算法

e.Continuous(rolling)budgets

连续(滚动)预算

f.Flexible budgeting

弹性预算

5.Annual profit plan and supporting schedules

年度利润计划和附表

a.Operational budgets

营业预算

b.Financial budgets

财务预算

c.Capital budgets

资本预算

6.Top-level planning and analysis

顶层规划与分析

a.Pro forma income

预计损益表

b.Financial statement projections

预计财务报表

c.Cash flow projections

预计现金流量

Institute of Certified Management Accountants

C.Performance Management(20%-Levels A,B,and C)

绩效管理(20%-A、B和C级)

1.Cost and variance measures

成本与差异核算

a.Comparison of actual to planned results

实际结果与预期结果对比

b.Use of flexible budgets to analyze performance

使用弹性预算分析绩效

c.Management by exception

例外管理

d.Use of standard cost systems

标准成本系统的使用

e.Analysis of variation from standard cost expectations

对预期的标准成本的差异分析

2.Responsibility centers and reporting segments

责任中心和报告部门

a.Types of responsibility centers

责任中心的种类

b.Transfer pricing

转移定价

c.Reporting of organizational segments

组织各部门的报告书

3.Performance measures

绩效考核

a.Product profitability analysis

产品获利能力分析

b.Business unit profitability analysis

经营单位获利能力分析

c.Customer profitability analysis

客户获利能力分析

d.Return on investment

投资回报率

e.Residual income

剩余收益

f.Investment base issues

投资基准问题

g.Key performance indicators(KPIs)

关键绩效指标

h.Balanced scorecard

平衡记分卡

Institute of Certified Management Accountants

D.Cost Management(15%-Levels A,B,and C)

成本管理(15%-A、B和C级)

1.Measurement concepts

计量概念

a.Cost behavior and cost objects

成本习性和成本对象

b.Actual and normal costs

实际成本和正常成本

c.Standard costs

标准成本

d.Absorption(full)costing

吸收(全部)成本法

e.Variable(direct)costing

变动(直接)成本法

f.Joint and by-product costing

联产品和副产品成本法

2.Costing systems

成本计算系统

a.Job order costing

分批成本法

b.Process costing

分步成本法

c.Activity-based costing

作业成本法

d.Life-cycle costing

生命周期成本法

3.Overhead costs

间接成本

a.Fixed and variable overhead expenses

固定和变动间接费用

b.Plant-wide versus departmental overhead

全厂间接费用和部门(车间)间接费用

c.Determination of allocation base

分摊基础的确定

d.Allocation of service department costs

服务部门成本的分摊

Institute of Certified Management Accountants

4.Supply Chain Management

供应链管理

a.Lean resource management techniques

精益制造资源管理技术

b.Enterprise resource planning(ERP)

企业资源计划

c.Theory of constraints

约束理论

d.Capacity management and analysis

产能管理和分析

5.Business process improvement

业务流程改进

a.Value chain analysis

价值链分析

b.Value-added concepts

增值概念

c.Process analysis,redesign,and standardization

流程分析,再设计,和标准化

d.Activity-based management

作业管理

e.Continuous improvement concepts

持续改进概念

f.Best practice analysis

最佳实践分析

g.Cost of quality analysis

质量成本分析

h.Efficient accounting processes

高效的会计流程

E.Internal Controls(15%-Levels A,B,and C)

内部控制(15%-A、B和C级)

1.Governance,risk,and compliance

管理,风险与法规遵守

a.Internal control structure and management philosophy

内部的控制结构和管理理念

b.Internal control policies for safeguarding and assurance

保护和保证的内部控制政策

c.Internal control risk

内部控制风险

d.Corporate governance

公司治理

Institute of Certified Management Accountants

e.External audit requirements

外部审计规要

2.Systems controls and security measures

系统控制和安全措施

a.General accounting system controls

普通会计系统控制

b.Application and transaction controls

应用控制和交易控制

c.Network controls

网络控制

d.Backup controls

安全备份管控

e.Business continuity planning

业务连续性计划

F.Technology and Analytics(15%-Levels A,B,and C)

科技与分析(15%-A、B和C级)

1.Infor管理会计师ion systems

信息系统

a.Accounting infor管理会计师ion systems

会计信息系统

b.Enterprise resource planning systems

企业资源计划系统

c.Enterprise performance management systems

企业绩效管理系统

2.Data governance

数据管控

a.Data policies and procedures

数据政策和程序

b.Lifecycle of data

数据生命周期

c.Controls against security breaches

控制安全漏洞

3.Technology-enabled finance transfor管理会计师ion

技术支持的财务转型

a.System Development Life Cycle

系统开发生命周期

b.Process auto管理会计师ion

工序自动化

Institute of Certified Management Accountants

c.Innovative applications

创新应用

4.Data analytics

数据分析

a.Business intelligence

商业智能

b.Data mining

数据挖掘

c.Analytic tools

分析工具

d.Data visualization

数据可视化

相关拓展:

复制本文链接

复制本文链接 模拟题库

模拟题库

875

875

扫一扫

扫一扫

扫一扫

扫一扫